You don’t have to look far on the West Coast of Canada to see the impact that climate change and rising sea levels are having on our communities. “We can’t afford to wait. How financial institutions allocate capital will be pivotal in making sure we are part of the solution,” says Tamara Vrooman, president and CEO of Vancity. “To make informed decisions about how we allocate capital, we first need credible, standardized ways to understand and measure the impact of our loans and investments on people, planet and long-term prosperity.”

Vancity is a values-based financial co‑operative located in British Columbia, Canada, serving the needs of more than 530,000 member-owners and their communities across 59 branches. Vancity has been tracking, reporting and growing the percentage of our assets that meet triple bottom line criteria since 2011.

However, collecting consistent and timely data that enables us to track actual social and environmental outcomes as a result of the lending we do continues to be challenging. This is why Vancity joined the Partnership for Carbon Accounting Financials (PCAF) in March 2019. Shortly afterwards, we signed onto the Global Alliance for Banking on Values’ Climate Change Commitment and the United Nations’ Principles for Responsible Banking and Collective Commitment to Climate Action.

Through these initiatives we are committed to disclosing the climate impact of our loans and investments, and to setting targets that align our portfolios with the goals of the Paris Climate Agreement. PCAF provides methodologies for financial institutions to measure the emissions financed through loans and investments.

As a member of PCAF North America, Vancity contributed to the adaptation of the methodology to the North American context originally developed by PCAF Netherlands, and led the development of the approach to measure the greenhouse gas emissions associated with residential mortgages. The methodology allows us and other financial institutions to generate the foundational data needed for the work that necessarily follows—to ultimately ensure that the loans and investments we make align with the goals of the Paris Climate Agreement.

In 2020, we applied the PCAF methodology to Vancity’s residential and commercial mortgages and motor vehicle loans, and to the investment funds we manage on behalf of members and clients through our subsidiary Vancity Investment Management. We plan to apply the methodology to our business loans shortly using the web-based Emissions Factor Database recently developed by PCAF.

In this case study we would like to showcase our carbon accounting work on residential mortgages.

Vancity’s residential mortgages portfolio covers single-family detached homes (SFDH), single-family attached homes, and apartments. We use SFDH as our example below, but we applied the same process to all three segments of the portfolio.

First, from the Natural Resource Canada (NRCAN) database we obtain total emissions in British Columbia attributed to SFDHs as well as the total stock (number of) of SFDHs in British Columbia.

Then, from our internal databases we collect the number of SFDH collaterals we have on our books. It required significant effort to get to this step, but now that the process is established we expect future calculations to be relatively straightforward.

The calculation is as follows:

While the NRCAN data excludes Scope 1 building’s emissions associated with electricity use, it does include building’s electricity consumption in petajoules (PJ). In order to obtain emissions generated by electricity consumption, we collect GHG intensity data (tCO2e/GWh) from BC Hydro and complete the following calculation:

We add up these two figures to estimate total tCO2e for SFDHs: 63,601 tCO2e.

We complete this process for the other two housing types: single-family attached homes and apartments. In this way we arrive at a total of 85,589 tCO2e.

To get relative figures, we simply divide total tCO2e by total dollars invested in this asset category. We were able to map 96% of our residential mortgage portfolio of $11.98 billion, so we apply this portion to the total value of the portfolio (96% * $11.9 bil CAD) to determine the denominator.

Summary of Results:

Per the PCAF methodology, greenhouse gas emissions are based on the annual energy use of the home (i.e. Scope 1 and 2 emissions of the building). The methodology excludes other annual GHG emissions and embodied emissions, such as emissions generated during the extraction, manufacture and transport of building materials, as well as during the construction and through the end-of-life demolition. The idea is that these emissions would be attributed to loans provided to the companies in construction and manufacturing sectors, etc.

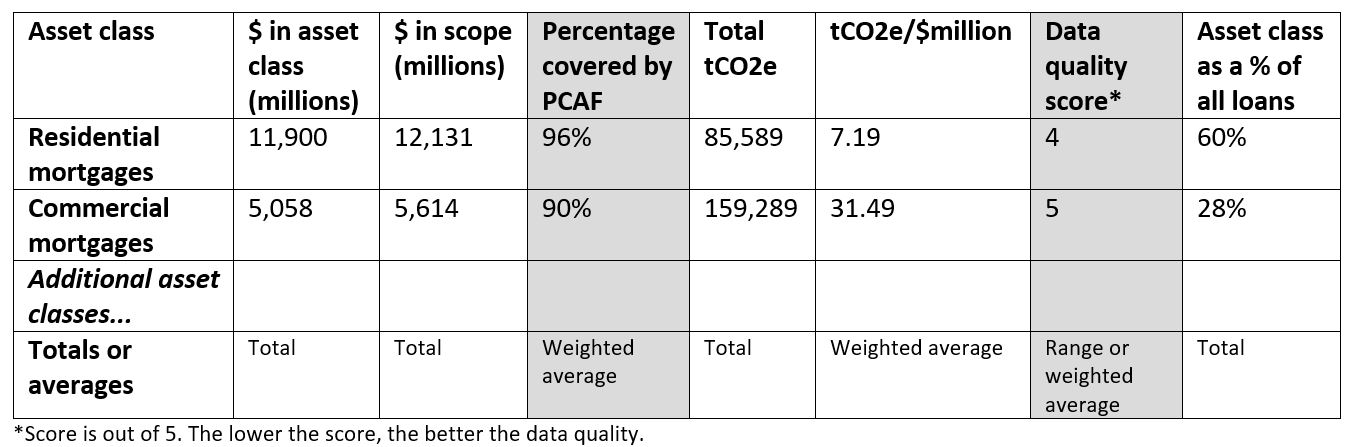

The following is a suggested template for publicly reporting results. It can be adapted by organizations as needed. It includes key elements that need to be reported including the data quality score and the percentage of the asset class covered by the PCAF methodology.

Our preliminary results are based on highly estimated data – our data quality scores are 4 or 5. As such, the data is limited in its application, especially for strategic decision making and tracking reductions as a result of specific products and initiatives.

However, the results provide us initial insights into the relative sizes of financed emissions for each asset class in relation to each other, compared to our operational emissions, and compared to other financial institutions that have also chosen to share or publish their results. As you can see from the table above, we can now understand that the climate impact of commercial mortgages is more than four times that of a residential mortgage per million dollars invested. Such insights have already led to some interesting conversations about implications and potential strategies.

For mortgages that provide financing to individuals or organizations to construct, buy, or renovate real estate, we rely on annual emission estimates by housing type provided by NRCAN (Natural Resources Canada). Ideally, we would be able to leverage actual building emissions data, or failing that, building energy labels. In the meantime, data for the square footage of the buildings we finance and building heating types will further improve our data accuracy.

As our data quality improves, we recognize that we may have to restate baseline/historical data in order to accurately depict our progress over time. However, we need to start somewhere. We feel strongly that poor data quality should not be used as an excuse to delay tracking and disclosing financed emissions from loans and investments. Collectively, we need to be more comfortable reporting imperfect data, and to potentially restating historical results as the data quality improves. This is why it will be important to have consistent and transparent rules for disclosure and incorporating data improvements over time.

Vancity’s focus over the coming months will be to identify ways we can enhance the availability and quality of emissions-related data for “material” asset classes and/or loan types. This work could include:

We will continue to advance Vancity’s programs to achieve systems-level change in regional emissions reductions, along with economic inclusion and enhanced community wellbeing. Measures we are taking include strategic partnerships, granting programs, education and training programs, modelling best practices, advocacy within sectors, validating early stage innovation, and new funding and financing models. We’re focused on three key areas: green and net-zero emission buildings, including deep energy retrofits; ensuring a just transition by integrating efforts on affordable housing and climate action; and promoting “lighter living” with our staff and members, and across our communities.